Markets··5 min read

Airlines Just Got a Fuel Tailwind — Oil's Weekend Crash Explained

Ruslan Averin on July 27: Brent crashed below $90 after the US–Iran pause, and airline stocks led the relief rally. Why fuel is the whole trade.

Notes on equities, options strategies, and market analysis.

Ruslan Averin on July 27: Brent crashed below $90 after the US–Iran pause, and airline stocks led the relief rally. Why fuel is the whole trade.

Ruslan Averin on the cruise-line pop: as Brent crashed below $90, Norwegian and peers jumped on fuel relief. The margin math — and the catch.

Ruslan Averin on BlackRock's Q2: record $15.3T in assets, a 10% EPS beat, and $199B of inflows. Why the flows matter more than the print.

Ruslan Averin on CME Group's record H1 2026: $2.99 EPS beat, record market-data revenue, and why the exchange model thrives on the chaos.

Ruslan Averin on General Motors' Q2: $3.57 EPS beat $3.20, revenue topped $48B, and management raised full-year profit guidance. The read.

Ruslan Averin on AT&T's standout quarter: its strongest earnings beat in years on subscriber and fiber momentum. Why the cash flow is the story.

Ruslan Averin on the CLARITY Act catalyst: with a Senate vote looming and meme coins surging, why regulatory clarity — not price — is Coinbase's real driver.

Ruslan Averin on gold near $4,100: why the metal rose as oil crashed, how far it fell from January's record, and what it says about the Fed.

Ruslan Averin on Alphabet: Q2 capex hit $44.9B and the full-year outlook rose again. Shares slipped below the 100-day average as free cash flow fell 47%.

Ruslan Averin on the semis-to-hyperscaler rotation: the chip index fell hard in July after doubling in the first half. What that rotation is actually pricing.

Ruslan Averin on oil at $100: Brent is up 37% from its June low as the Iran war escalates, and Treasury yields are at the year's highs. That combination has a name.

Ruslan Averin on tanker economics: when routes lengthen and war-risk premiums rise, shipowners are paid on day one — regardless of where crude finally settles.

Ruslan Averin on domestic US producers: they receive the same crude price as everyone else, without the transit risk that produced it. That asymmetry is the trade.

Ruslan Averin on rates: yields at the year's highs while equities fall is not a growth scare. It's the bond market saying inflation, not weakness, is the binding constraint.

Ruslan Averin on IREN: shares jumped 26% as $2.8B in new AI-cloud contracts and an NVIDIA 5GW partnership take the GPU-financing risk off the table.

Ruslan Averin on SanDisk (SNDK): the pure NAND play surged ~14% after Morgan Stanley called for memory prices to rise 25% into Q3 on a data-center shortage.

Ruslan Averin on Super Micro (SMCI): shares surged ~20% after preliminary Q4 gross margin guidance jumped to 15-17% from 8.2% and orders topped $60B.

Ruslan Averin on Western Digital (WDC): the HDD maker rode the memory rally with all 2026 production sold out and cloud now 89% of sales on AI data-center demand.

Ruslan Averin on Micron (MU): the trillion-dollar memory maker with HBM sold out through 2026 and a multi-year Anthropic supply deal, riding a record Q3.

Ruslan Averin on Frontline (FRO): the largest listed VLCC operator — day rates explode when Hormuz is disrupted, booked at $181,700/day for Q2. A pure spot-rate bet.

Ruslan Averin on Cheniere (LNG): the largest US LNG exporter — the energy-security supplier when Hormuz chokes ~20% of world LNG, though spot upside is capped.

Ruslan Averin on RTX (Raytheon): a Hormuz conflict burns interceptors — Patriot, SM-3/6, Tomahawk — RTX restocks them on a record $271B backlog. But not cheap.

Ruslan Averin on Occidental (OXY): the analysts' geopolitical hedge — a US Permian barrel that captures a Hormuz oil spike with zero Strait transit risk.

Ruslan Averin on Lockheed Martin (LMT): it builds THAAD and PAC-3 — the interceptors the Gulf runs out of — yet down 25%. Same demand as RTX, half the multiple.

Ruslan Averin on Veralto (VLTO): the water-quality compounder spun from Danaher — a razor-and-blade model, PFAS tailwind, and why quality costs 24x earnings.

Ruslan Averin on Mueller Water Products (MWA): a $4B small-cap making valves and hydrants — a near-pure-play on federally funded U.S. water-pipe replacement.

Ruslan Averin on California Water Service (CWT): a 59-year Dividend King whose $0.07 quarter was pure regulatory lag — and why the rate case is the real catalyst.

Ruslan Averin on American States Water (AWR): the longest dividend-growth streak on the NYSE — 71 years — and the military-base contracts almost nobody prices in.

Ruslan Averin on Energy Recovery (ERII): a near-monopoly on the energy-saving heart of seawater desalination — trading near lows amid a self-inflicted reset.

Ruslan Averin on Morgan Stanley's record Q2: profit up 58% to $5.58B, record equities trading, a $20B buyback — and why the beat's quality matters most.

Ruslan Averin on TSMC's June sales up 67.9% and first-half revenue near $75B — the clearest read that AI infrastructure demand is accelerating, not peaking.

Ruslan Averin's call on Meta — at a forward P/E of 17.6 the market prices its $145B AI capex as value destruction. The July 29 Q2 print is the catalyst.

Ruslan Averin's read — Tesla closed at $396 on June 17, down 2%. Deliveries are tracking ahead of consensus, but a 385x earnings multiple leaves no room for error. Here's the price I'd actually pay.

Ruslan Averin's read — GM crushed Q1, shrank its EV losses, raised guidance and launched a $6B buyback — yet trades at 8x earnings. At $80 after a 3.5% pullback, this is the auto name I'd actually buy.

Ruslan Averin's read — Ford pays a 4% yield and beat Q1, but a 180K-vehicle recall and a sharp June sales drop just knocked it to $13.96. The income is real; the quality is the question.

Ruslan Averin's read — Rivian popped 7% as the first R2 SUVs rolled off the line. The product is real and the cash burn is shrinking — but it's still unprofitable. Here's the level I'd risk capital.

Ruslan Averin's read — Lucid did a 1-for-10 reverse split just to stay listed, and the stock fell again. Great cars, broken stock. This is the one auto name on my avoid list.

Ruslan Averin's read — Toyota's ADR sits at $173, near its 52-week low, after U.S. tariffs cut operating income 21%. At 9x earnings with a 3.1% yield and a $256 Street target, this is the value play in global autos.

Ruslan Averin's read — Honda's ADR is down 21% this year to $26, paying a 3.9% dividend while trailing income turned negative on tariffs. The Nissan merger collapsed. Is the income enough to own it?

Ruslan Averin's read — Nissan is cutting 20,000 jobs, posted a ¥533B loss and suspended its dividend. The 'Re:Nissan' turnaround may eventually work, but at ¥350 this is a restructuring bet, not an investment.

Ruslan Averin's read — Hyundai's profit fell 24% on U.S. tariffs, yet revenue hit a record and hybrids jumped 32%. With 26 analyst Buys and zero Sells, this is the quiet quality name in global autos.

Ruslan Averin's read — Ferrari has fallen from $519 to $354, dragged down with the auto sector it barely belongs to. With a Strong Buy rating and a $439 target, this is the highest-quality name on my buy list.

Ruslan Averin's read — Volkswagen trades at 7x earnings with a 6% dividend after tariffs and a China slump cut Q1 profit 14%. With 30+ new China NEVs coming and a €111+ target, the value case is loud.

Ruslan Averin's read — BMW slashed its 2026 guidance on June 17 and the stock dropped 8%, dragging the whole sector. At ~6x earnings with a 6.3% yield, it's cheap — but cheap on numbers that just moved.

Ruslan Averin's read — Mercedes sits at a 52-week low near €47 as China sales fell 27% and management calls 2026 a 'rebuilding period.' The 7.2% dividend is the draw — if it holds. Here's my level.

Ruslan Averin's read — Porsche AG is the lone European auto gainer in 2026, up 7% near its highs — yet it just warned on earnings, trades at 143x, and slashed its EV plans. Strong brand, wrong price.

Ruslan Averin's read — Stellantis returned to profit in Q1 but trades at $6.47 with an 8.9% dividend after a $25B 2025 loss. When a yield is this high, the market is telling you it doubts the payout.

Ruslan Averin's read — Renault is down ~30% to €27 after a €9.5B Nissan-stake write-down and a strategy reset that killed the Ampere EV IPO. The 7.9% yield tempts, but this is a 'show me' story.

Ruslan Averin's read — BYD's overseas sales hit a record 160,000 units in May, up 80%, yet the stock is down 26% on a brutal China price war. At HK$82 with a HK$125 target, this is my top Chinese pick.

Ruslan Averin's read — Li Auto, once the profitable Chinese EV, slipped to a quarterly loss and sits at its 52-week low of $13.58. The new L9 and a Q2 delivery rebound could turn it — but I need proof first.

Ruslan Averin's read — NIO's May deliveries hit a record 37,705, up 62%, yet the stock is flat at $5 and still loses money on every car. A Pentagon designation dispute adds risk. This stays speculative.

Ruslan Averin's read — XPeng's exports jumped 80% and its X9 just launched across Europe, but total deliveries fell for a fifth straight month and it's down 31% to $13. A $23 target tempts — with real risk.

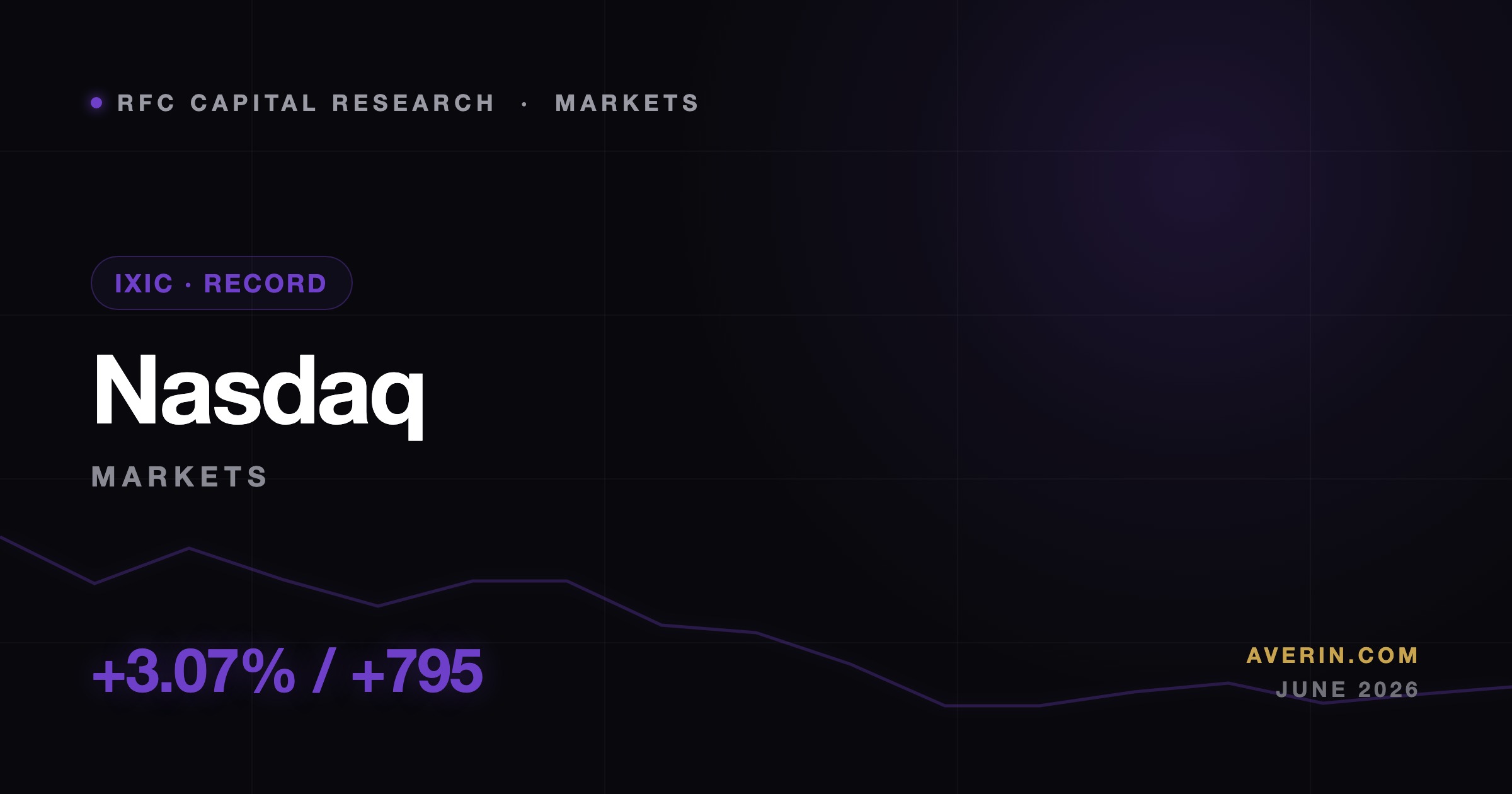

Ruslan Averin’s read — The Nasdaq jumped 3.07% to 26,683 on June 15, nearly triple the Dow's gain. My take: lower oil and lower yields are rocket fuel for long-duration growth — and SpaceX didn't hurt.

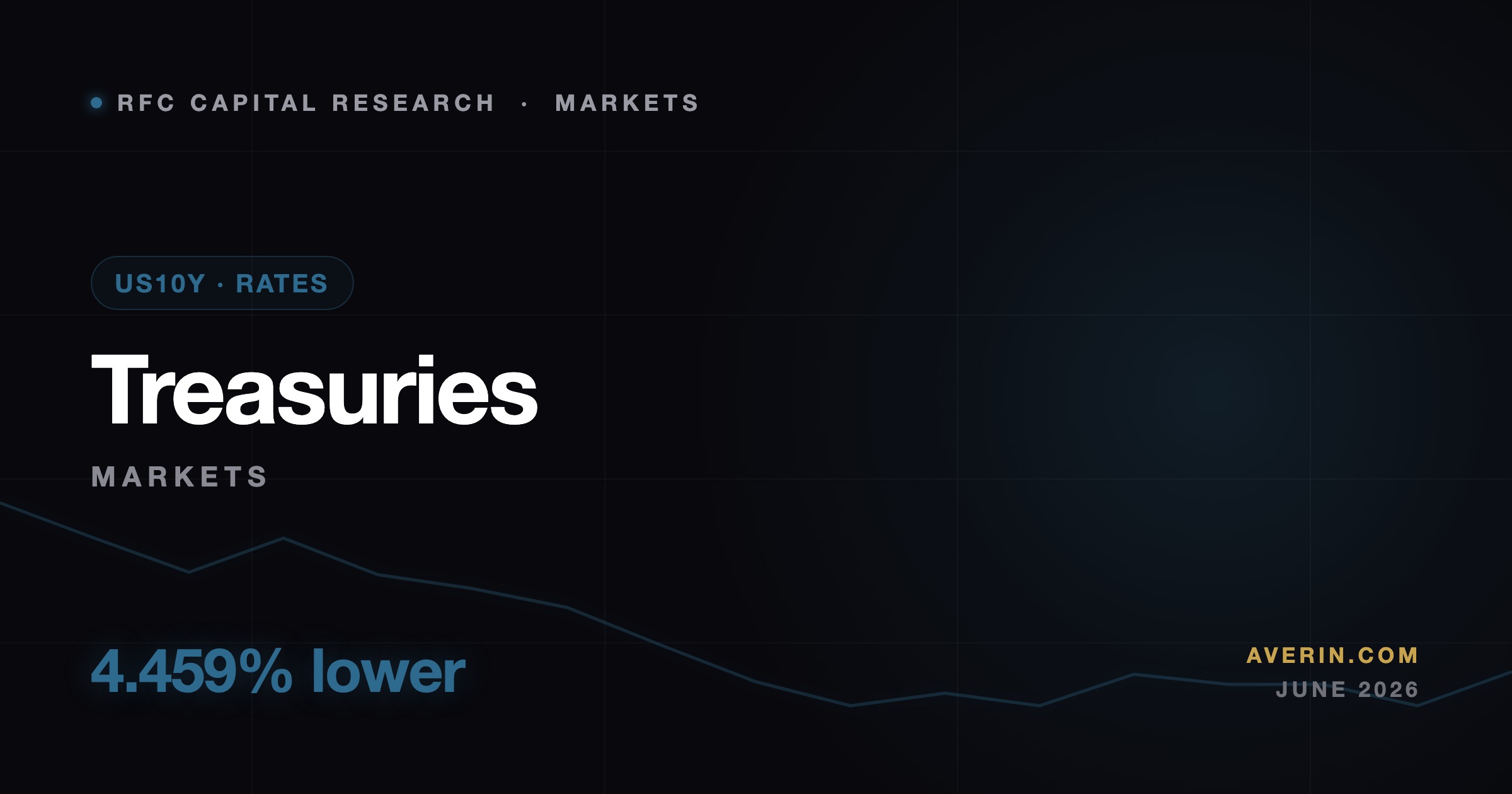

Ruslan Averin’s read — The 10-year yield slipped to 4.459% as the Iran deal reshaped the rate outlook. My take: the bond market's quiet move is the cleanest signal of what actually changed on June 15.

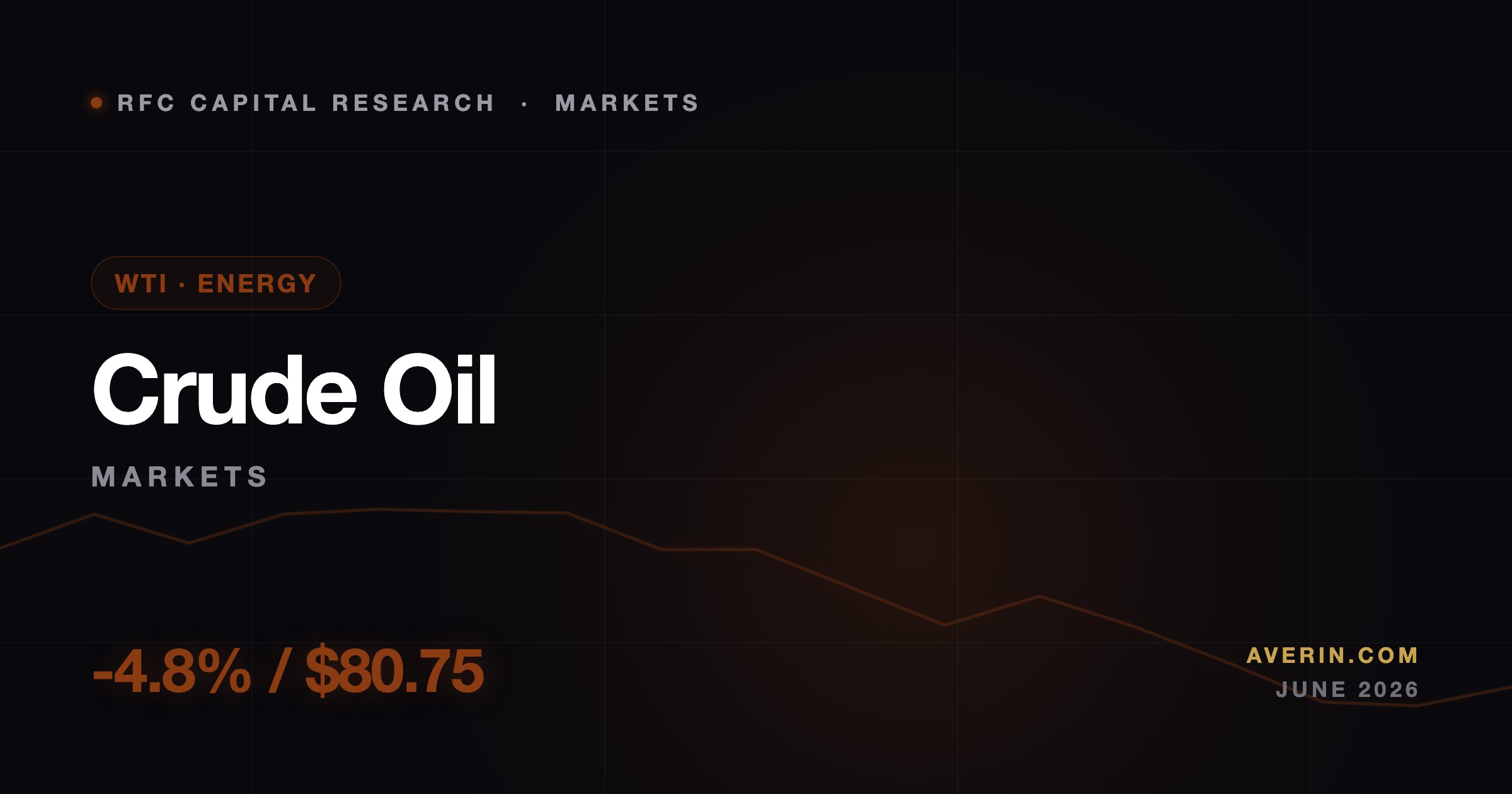

WTI fell ~4.8% to $80.75 as the Strait of Hormuz reopens. Ruslan Averin's read: the oil move is the single most important number from June 15 — and it's not really about energy stocks.

SPCX climbed 20% on Monday to close at $192.50, its first full day of trading after the largest IPO in history. As an analyst, Ruslan Averin breaks down why the move is real and where the float math gets dangerous.

The Nasdaq jumped 3.07% to 26,683 on June 15 after the U.S. and Iran announced a deal to end the war and reopen the Strait of Hormuz. Ruslan Averin maps who led the risk-on leg and why oil's drop matters more than the headline.

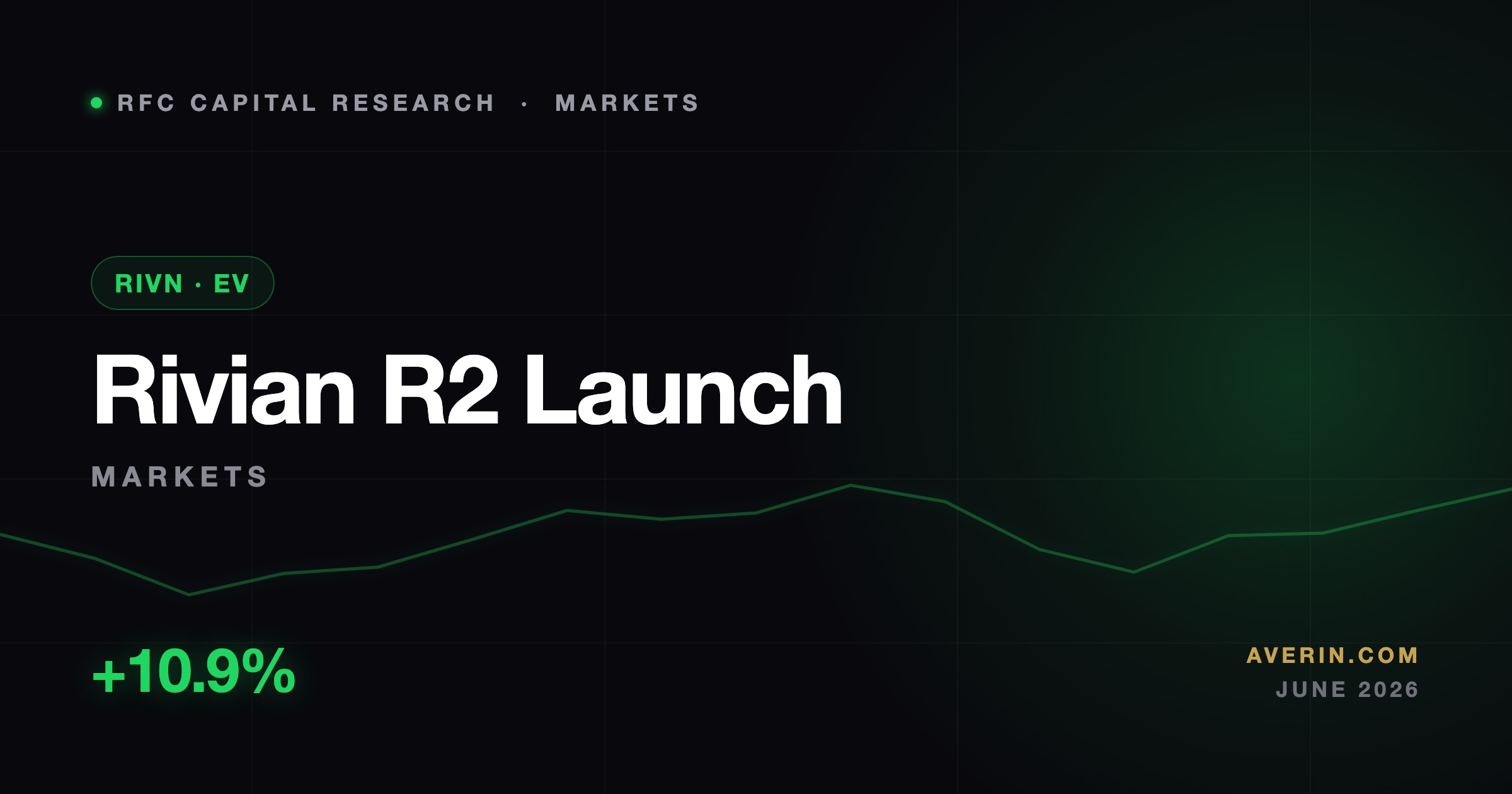

RIVN traded up 7.25% on June 12 as the first public R2 deliveries began and an AT&T 5G deal landed. Ruslan Averin explains why the delivery candle is the easy part — and what Q2 has to prove.

Gold rose 2.81% to $4,357 on June 15 even as a U.S.–Iran ceasefire sent stocks toward records. Ruslan Averin on why safe havens rallied into good news — and what the bond market is really pricing.

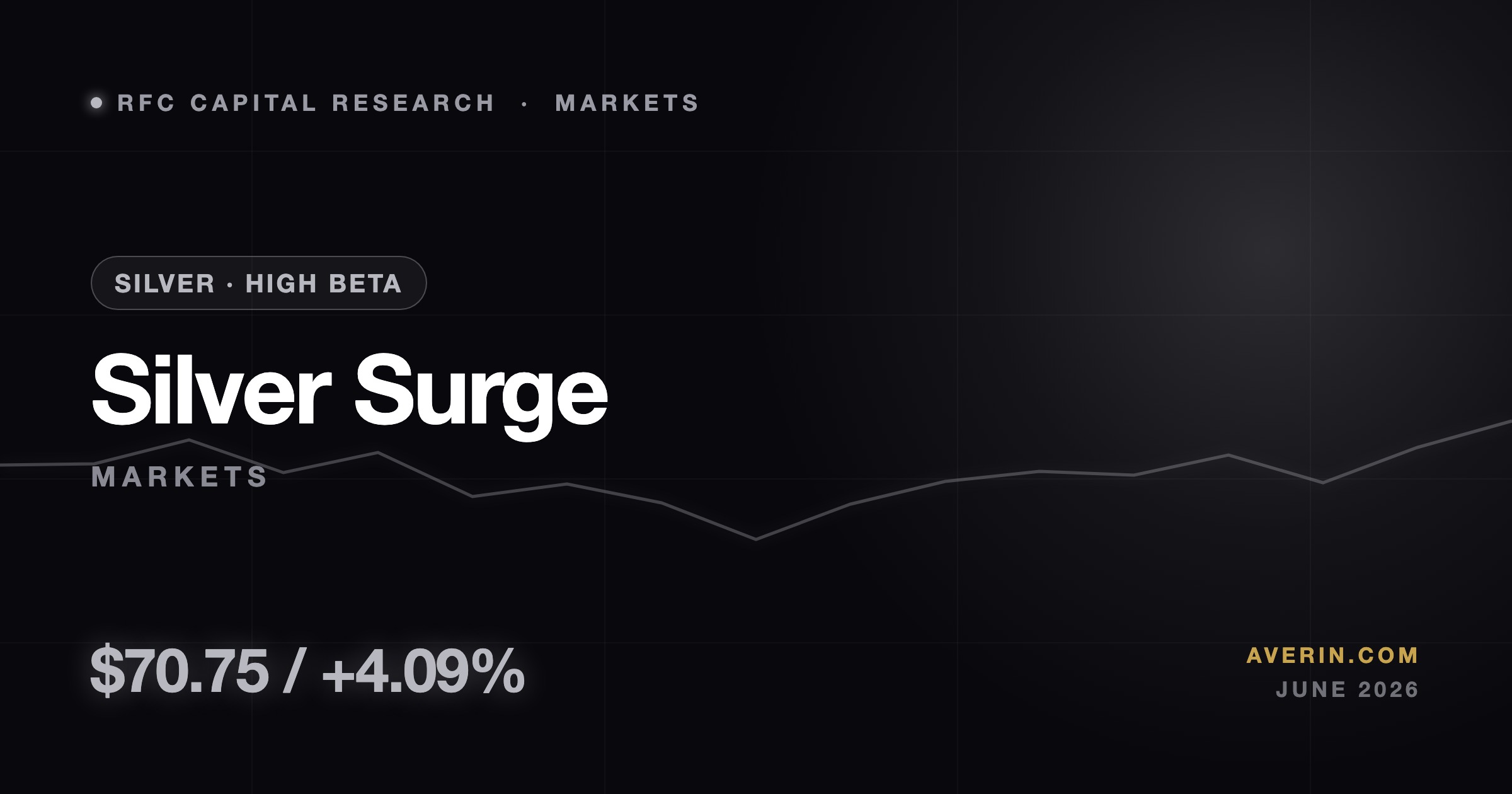

Silver surged 4.09% to $70.75 on June 15, outrunning gold's 2.81%. Ruslan Averin on the gold/silver ratio, silver's 100%+ year, and whether the higher-beta metal is a buy or a warning.

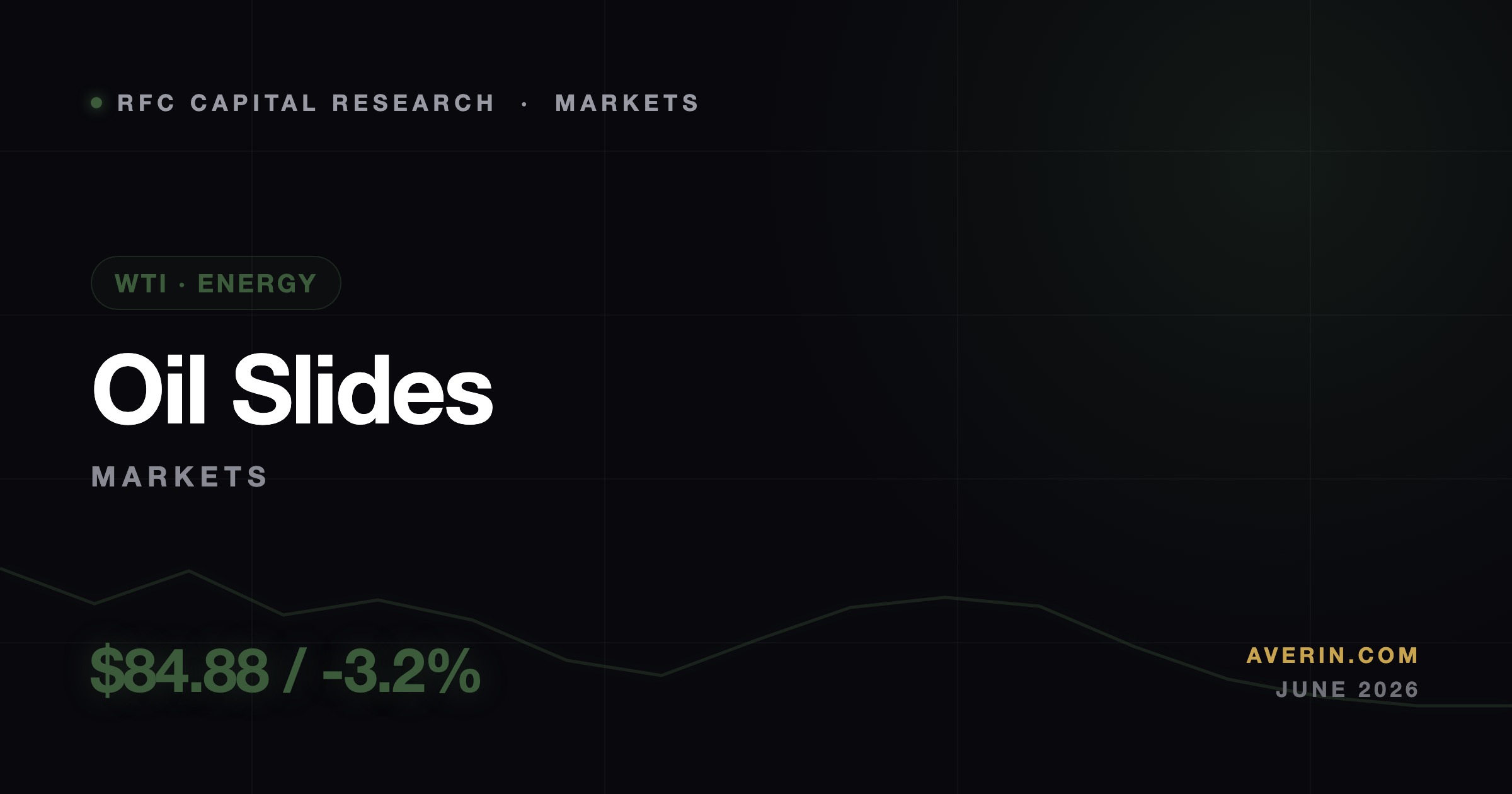

WTI dropped 3.2% to $84.88 and Brent fell 3.4% as a U.S.–Iran ceasefire reopened the Strait of Hormuz. Ruslan Averin on the energy read-through and where the risk premium goes next.

The VanEck Gold Miners ETF jumped 8.26% on June 15 — nearly triple gold's spot move. Ruslan Averin on operating leverage, why miners finally caught the metal, and the risk in chasing them.

Rivian climbed off its lows during the June 15 risk-on rally as the R2 SUV launch reframes the whole story. Analyst Ruslan Averin breaks down whether mass-market volume finally justifies the move.

The June 15 peace-deal rally lit up the riskiest corners of the market, and small caps have quietly led all year. Analyst Ruslan Averin on why the Russell 2000 is the tell to watch.

Small-cap momentum names like AXT and Seagate ripped on June 15 as risk appetite surged. Analyst Ruslan Averin on the one question to ask before chasing any double-digit mover.

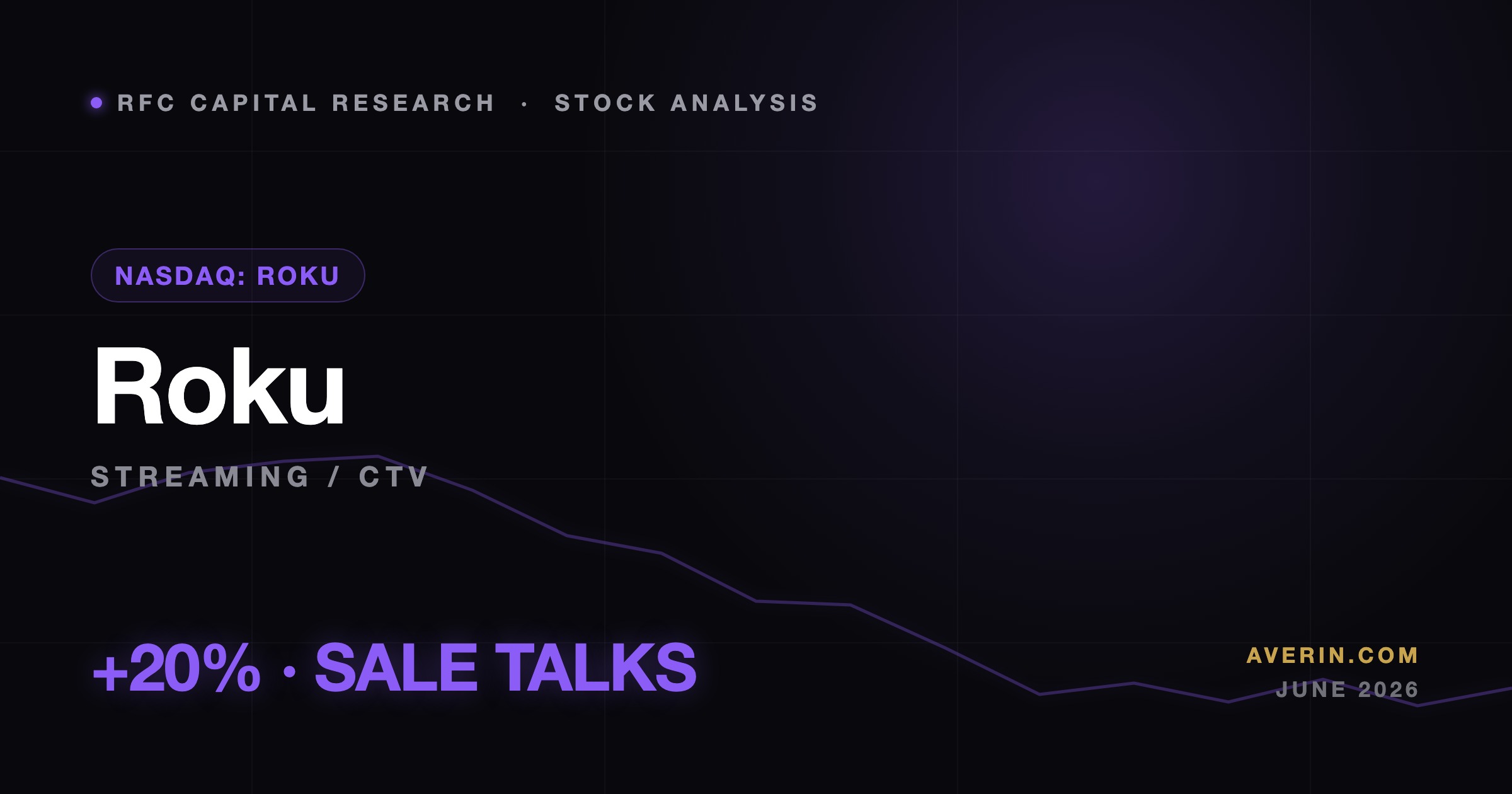

Roku surged 20% on June 12 on a report it is in sale talks with a U.S. media company — with an S&P MidCap 400 add on June 22 and target hikes stacked behind it.

Rivian rose 7.9% on June 12 as R2 SUV deliveries began and VW's stake topped 15% — but a new NHTSA probe of 114,000 vehicles is the risk nobody is pricing.

Tesla closed up 1.8% on June 12 in the glow of SpaceX's historic IPO, an unsupervised Austin robotaxi rollout, new EU FSD approvals and a JPMorgan upgrade.

Riot rose 1.8% on June 12 as its bitcoin-to-AI pivot matured — $33.2M in first data-center revenue and a 10-year AMD lease scaling toward 200 MW.

AT&T and Verizon each rose ~2.5% on June 12 — a telecom-led session where a 6% Verizon yield and AT&T's deleveraging story signal a rotation into defensives.

Microsoft and Amazon lost $350B+ each, Apple and Alphabet ~$300B, Nvidia $260B — $2 trillion gone from the Mag 7 in June while the median S&P stock is actually up. This is a leadership problem, not a market problem.

US airstrikes on Iran, CPI at 4.2% — and gold fell 0.9% to its lowest open since November 2025. The safe haven that ignores war is telling you what it actually fears: the Fed.

The S&P 500 fell 2.5% this week to 7,383.74, its first weekly loss in 10 weeks. A strong May jobs report revived rate-hike fears. Here is how I read the regime.

Opened a long position in iShares Semiconductor ETF at $547.20 on May 23. Closed today at $563.98. Net gain: +$16.78 per share. Full trade breakdown and exit reasoning.

Opened SMCI long at $36.00 on May 23. Closed today at $38.19. Net +$2.19 per share, +6.1%. The highest return in the May 25–28 book. Full breakdown.

Opened a short on Charles Schwab at $88.50 on May 23. Covered today at $85.61 as SCHW dropped 4.24% in a single session. Net gain: +$2.89 per share. Full trade breakdown.

Opened a short on SBSW at $12.00 on May 23. Covered today at $11.86 as the platinum miner dropped 2.47% on May 28. Net +$0.14 per share. Why I shorted a commodity name.

Opened a long on Regions Financial at $27.80 on May 23. Closed today at $28.09. Net +$0.29 per share (+1.04%). Why I use sleepy regional banks as portfolio ballast.

Opened a long on Prudential Financial at $101.00 on May 23. Closed today at $101.49. Net +$0.49 per share (+0.49%). Why I close a dividend position after three days and what the Japan angle was.

Opened PFE long at $25.50 on May 23. Closed today at $26.21 as Pfizer gained +1.39% on the day against a weak tape. Net +$0.71 per share (+2.78%). Why contrarian pharma worked this week.

I spend 5 hours every Sunday preparing for the trading week. Hour-by-hour breakdown: macro review, IV scan, chart review, position audit, trade plan writing.

I never risk more than 3% on a single trade. My conviction-tiered sizing system, Kelly sanity check, and sector correlation rules — the complete framework.

Every Friday I filter S&P 500 + Nasdaq 100 through 5 screens to find 5 high-conviction names. Relative strength, liquidity, fundamentals, earnings transcript language.

Retail ETF XRT fell 6%+ in one week — its 4th straight weekly decline. Credit card delinquencies at 3.2%, real wages squeezed. Here's how I'm repositioning.

Brent crude is at $105 — 40% above pre-conflict levels. Ten of the last twelve recessions were preceded by oil price spikes. Here's why markets are underpricing this signal.

10-year Treasury at 4.56% with CPI at 3.8% leaves a real yield of just 0.76%. Add Warsh's rate hike odds and the bond math for Q2 2026 gets more complex than the headline suggests.

S&P 500 set a new all-time high at 7,444 on May 14. But April PPI came in at +1.4% vs 0.5% estimate — a divergence that explains why the Dow fell the same day.

Dow +1,100 points, S&P +3%, Nasdaq +3.2% on the US-China tariff pause. Why the rally is real — and why it's not the signal most people think it is.

DAX surged past 25,000 for the first time in history in early 2026. Here's why European equities offer a compelling case vs. a stretched S&P 500.

78% of S&P 500 companies beat Q1 estimates. EPS grew 9.4% YoY, led by tech and financials. Here's what the earnings picture tells me about the second half of 2026.

DXY dropped below 100 for the first time since 2022. The implications for international equities, commodities, and dollar-denominated debt are larger than most investors realize.

EM equities trade at 12x forward earnings vs 21x for the S&P 500. Dollar weakness is the catalyst. I'm building positions in EEM, VWO, and India-specific exposure.

S&P 500 hit ATH 7,230 on April 30. EPS beat rate 84%, blended growth +27.1%. Both bulls and bears have a case — here is how I read it.

SPX bounced 12% from April lows, VIX fell to 22. Here's what the numbers tell us about May.

Q1 GDP at 0.5%, Brent above $107 with Hormuz closed, Fed chair transition — three shocks converging. Here's what I'm watching and where I'm positioned.

DXY below 98.4 for the first time since 2022 changes everything — I trimmed USD cash 8 points and redeployed into gold, EM equities, and commodity.

Bond market 2026 outlook: Fed on hold at 3.50-3.75%, 10-year at 4.3%. Investment grade and high yield offering best risk-adjusted entry in a decade.

Gold at $4,800, Brent above $100, and the dollar weakening — how commodities fit into my portfolio and what I'm doing about it.

Nvidia vs Cisco dot-com bubble comparison: $690B hyperscaler capex, 71% gross margins, and real earnings. Here's where the AI trade is bubble — and where it isn't.

The DAX at 17x earnings while the S&P trades at 21x. European defense spending is booming, banks are flush, and nobody in the US is paying attention. That's exactly why I'm buying.

Wars, tariffs, elections, oil blockades — the geopolitical risk menu is the thickest I have seen in my career, and most investors are pricing almost none of it.

SpaceX options just listed with no IV history, so the premium is huge. The bull put spread lets you sell that fear with maximum loss known to the penny.

SpaceX stock looks expensive at 190. Instead of chasing it, sell a cash-secured put and get paid to buy lower — the inflated IPO premium funds the wait.

If you own SpaceX stock, the fat new-listing call premium is income on the table. The covered call harvests it; the wheel turns it into a monthly engine.

A SpaceX iron condor sells both sides of the inflated IV with defined risk. But a small float and upside squeeze risk are why I keep this one tiny.

SpaceX options are live with triple-digit IV and wide spreads. Here is the full safety-first playbook for selling that premium — ranked by risk, with rules.

After 10 weeks of grind-up calm, implied volatility was priced for complacency. Then payrolls came in at 172K and the VIX spiked. Here is how I read cheap protection before a known catalyst.

I target portfolio delta between -0.05 and +0.05 with $50-200/day theta. When delta drifts past ±0.10, I rebalance. My thinkorswim setup and real rebalancing example.

My earnings options framework: buy straddles pre-earnings when IV rank <40, sell post-earnings CSPs when IV is still elevated. Two NVDA trades — one loss, one win.

I use cash-secured puts in 3 scenarios — overvalued stock I want, post-earnings elevated IV, oversold conditions. My AAPL example: $3.20 collected, $196.80 effective cost.

When a trade loses I follow a 3-threshold protocol: -25% review, -50% consider rolling, -100% close no exceptions. The NVDA iron condor that forced this system.

I sell covered calls on 4 dividend stocks — JNJ, PG, KO, XOM — generating 1.14%/month on top of dividends. My exact selection criteria and setup.

I trade iron condors with 7 non-negotiable rules. IV rank, strike selection, width math, and profit management — my complete neutral-market framework.

I trade VIX spikes above 25 with a 3-step system: IV rank scan, put credit spreads at -1σ, close at 50%. Here's the exact setup I use.

Q1 2026 options ADV reached 68.6M contracts/day — a new record. Here is what the surge in 0DTE retail volume and institutional hedging signals going into May expiration.

May 21 brings 51 earnings reports in a single day. VIX at 18, IV crush risk up to 60% post-release. Here's my playbook for straddles, iron condors, and the NVDA calendar spread.

VIX closed at 17.99 while CPI hits 3.8% and PPI +1.4%. Four Fed dissents. Traders pricing 30% rate hike odds. My thesis: vol is too cheap for this macro setup.

My personal framework for options in 2026: the 3 setups I trade, how I size positions, what I avoid, and why high-IV semis are the most interesting market right now.

Micron options volume hit $2.8B in one session — more than SPY and QQQ combined. Here's what the trade says about the NAND supply chain and the week ahead.

NVDA reports May 20. IV is 40–55% before earnings, then collapses. Here's how to trade it without getting crushed.

The iron condor profits when a stock stays range-bound. Combine a bear call spread and a bull put spread to collect premium and let time work for you.

Stop-loss orders are free but gap down overnight and execute at terrible prices. Protective puts cost money but guarantee your exit. Here's how to choose.

Studies show 75% of options traders lose money in their first year. Here are the 10 mistakes that cause most of those losses — and exactly how to fix them.

The options chain looks like a wall of numbers. After this guide, you'll read it like a map — understanding every column from bid/ask to the Greeks.

A bull call spread lets you bet on a stock rising while capping both your maximum profit and loss — perfect for beginners who hate surprises.

Bear put spread profits from falling prices at a fraction of the cost of buying a put outright — with strictly capped risk.

Writing covered calls turns idle stock holdings into monthly income. Learn how to choose the right strike, calculate your yield, and manage the risk of having.

Learn how to collect premium income while waiting to buy your favorite stocks at a lower price — the same strategy Warren Buffett used to earn $7.5 million.

IV crush wiped out profits for traders who were right on direction but wrong on volatility. Here's everything beginners need to know about implied volatility.

Four numbers predict what your option does next. Learn Delta, Gamma, Theta, and Vega with real examples and a quick-reference table.

A practical walkthrough of buying a call option for the first time — from account approval to placing the trade and managing your position.

In 2022, the S&P 500 fell nearly 20%. Investors who held protective put options lost roughly half that. Here's how portfolio insurance with puts works — and.

Options let you control 100 shares of stock for a fraction of the price. Learn how calls and puts work with real examples and plain language.

An AAPL $200 call trading at $8.50 — where does that price come from? Learn the two components of every option premium: intrinsic value and time value.

Choosing the wrong strike price cost me $400 in my first options trade. Here's the framework I wish I had from day one.

VIX 17 + SKEW 141 + NVDA earnings May 20: three trades — QQQ covered call, iron condor, VIX calendar spread. Defined risk in a contradictory vol environment.

SMCI IV at 70% vs 159% realized vol — options priced for calm when the stock moves like a hurricane. The pre-earnings straddle setup explained.

I sold the May $250 covered call for $10.50 per share with IV at 31%. Effective cost basis: $216.90. Target: either 9.9% return at assignment or keep shares if.

VIX at 17.8 after six weeks of compression. NVDA earnings May 21. The pre-earnings vol expansion window is open — here is the setup.

Positioned a $412 straddle before MSFT earnings (April 30) for $18.40 per contract, betting on Azure growth re-acceleration or guidance disappointment.

Sold covered calls on AAPL at $204.80, capping upside at $210 while hedging against a worse-than-consensus China earnings miss.

VIX at 14.8 with SPX at 5,420 pricing in a Goldilocks scenario—no cuts, no hikes. I bought a June SPX put spread ($24 debit) to hedge equity book tail risk.

Four mega-cap earnings in one week, a Fed decision, and a GDP shock — all while VIX sits at 18. I'm not guessing direction. I'm collecting premium.

CAT hit a new all-time high of $845 on April 23. I was positioned long at $824 with a covered call at $840 — capped upside, but 3.1% in five sessions is.

HON beat Q1 EPS by $0.13 but missed revenue and guided Q2 below consensus. I opened a bear put spread at $215/$205 after the initial reaction faded. Sometimes.

XOM had been capped at $150 for several sessions while crude stayed indecisive. I entered at $146.80, sold the $150 covered call at $1.80, and closed the full.

FANG was $10 below its March high with no near-term catalysts in sight. I bought at $191.80 and sold the $195 call at $3.80 — the call expired worthless at.

VIX at 19, Iran war premiums elevated, earnings season in full swing — here is exactly what I am running and why.

Most retail traders use options to speculate. I use them to sleep at night.